2ND QUARTER 2016 RESULTS: EBITDA GROWTH ACCELERATES IN 2Q 2016

INTRALOT SA(RIC: INLr.AT, Bloomberg: INLOTGA),an international gaming solutions and operations leader, announces itsfinancial results for the six-month period ending June 30th, 2016, prepared in accordance with IFRS.

OVERVIEW

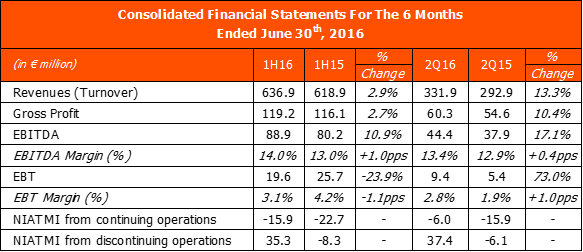

o Significant EBITDA growth of 17.1% in 2Q16 (+33.4% in constant currency); boosting 1H16 EBITDA increase to 10.9% (+26.0% in constant currency).

o EBITDA margin expanded by 50bps to 13.4% in 2Q16 and by 100bps to 14.0% in 1H16 compared to the corresponding periods of 2015.

o Group Revenues up 13.3% in 2Q16 (+26.2% in constant currency); bringing 1H16 revenues growth to 2.9% (+15.4% in constant currency).

o Adjusting for the effects from M&A transaction, net debt remained relatively stable for the third consecutive quarter.

o The Company took the following important steps in implementing strategic initiatives, which are in line with our strategy to create, in selected countries, strategic partnerships with strong local partners that offer substantial synergies and local market know-how, strengthening the development of the local business and to expand our gaming product portfolio:

In 2Q16 the merger of our Italian activities with Gamenet was completed.

In Peru we reached an agreement with Nexus Group to sell 80% of INTRALOT de Peru.

In July 2016 we completed the acquisition of a strategic stake in a leading gaming company in Bulgaria, Eurobet.

In August INTRALOT announced that it has entered into discussions with Tatts for a potential sale of INTRALOT’s Australian and New Zealand businesses.

New products and services that have been recently developed and installed to various clients include:

o Canvas, a proprietary CMS solution for online Betting, Lottery and Interactive Games

o Remote Gaming Server delivering e-Instants and Games on-Demand or on-Premise to clients

o Interactive Gaming Platform, a CRM platform segmenting and managing customer behavior

o Mobile applications (iOS, Android) with push notifications and real money gaming

o Self Service Terminals (SST), the next generation of self-service terminals for autonomous play, following the success of the first generation machines in the US

Notes:

1) The Group’s activities in Italy and those of Intralot de Peru SAC are presented as discontinued operations.

2) NIATMI from discontinued operations in 1H16 and 2Q16 includes a capital gain from the disposal of discontinued operations (merger) in Italy of €45.2m.

Commenting on the 2Q 2016 Results INTRALOT Group CEO Antonios Kerastaris noted:

“INTRALOT’s 2nd Quarter results reflect the impact of successful efforts in portfolio re-organization through a dynamic roadmap of new products and services and the geographical rebalancing of our presence, assisted by completed organizational changes and cost containment. We are particularly encouraged by high growth rates in mature markets such as the US as a clear sign of competitiveness gains and we are committed to further business development in North America and other promising regional markets such as Africa and East Asia. ”

OVERVIEW OFRESULTS

REVENUES

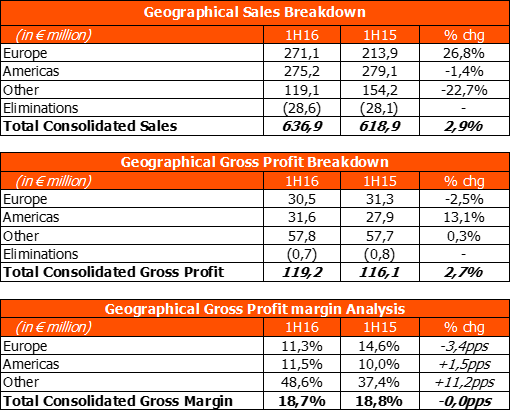

o Reported consolidated revenues increased by 13.3% to €331.9m in 2Q16 compared to the same period a year ago, shaping revenues in 1H16 to 636.9m or 2.9% higher y-o-y. Main growth areas in 2Q16 were the US, Turkey and Bulgaria.

o The increase in 1H16 derives from: +63.9m in East Europe due to increased sales in Bulgaria and Turkey, +19.3m in North America, +1.5m in Africa and +0.3m in West Europe, partially counterbalanced by decreased sales of 43.7m in Australasia due to lower sales in Azerbaijan where the local currency suffered severe devaluations last February and December and -23.3m in South America due to softer sales in Jamaica, Argentina and Peru.

o Constant currency basis: In 2Q16 revenues net of a negative FX impact of €37.8m reached €369.7m (+26.2% y-o-y), while in 1H16 revenues net of a negative FX impact of €77.1m shaped at €713.9m (+15.4% y-o-y).

o Numerical Games is the largest contributor to our top line, comprising 47.1% of our revenues (+5.2% vs. 1H15), followed by Sports Betting contributing 35.4% to Group turnover (-0.5% vs. 1H15). VLTs/AWPs represented 3.1% of Group turnover (+75.7% vs. 1H15), followed by Technology contracts with 11.9% (+5.7% vs. 1H15) and Racing with 2.5% (-34.2% vs. 1H15).

o Wagers handled

During the 1H16 period INTRALOT systems handled €12.3 bn. of wagers worldwide (from continuing operations), increased by 0.8% y-o-y. Africa increased by 21.1%, North America increased by 15.4%, East Europe increased by 3.1%, South America decreased by 13.6%, Asia decreased by 7.6% and West Europe decreased by 1.3%.

GROSS MARGIN / OPERATING INCOME / OPEX

o The Gross profit margin remained stable in 1H16 at 18.7% compared to 1H15, as margin expansion that took place in countries such as the US and Argentina was counterbalanced by margin contraction mainly in Bulgaria and Turkey. The payout ratio from continuing operations, in 1H16 increased by 3.2% vs. 1H15, while GGR increased by 2.8% (on a constant currency basis GGR increased by 14.3%). In 2Q16, the payout ratio increased by 4.0% vs. 2Q15, while GGR increased by 5.8%.

o Other operatingincome in 1H16 totaled€10.2m compared to €12.4m in 1H15, posting a decrease of 17.6%. The major drivers of this decrease were the non-recurring income in Australia due the operations sale in 2Q15 (€3.6m), partially offset by improved operations in Turkey (€1.6m) and the growth in instant ticket services of our US operations (€1.0m).

o Total operating expensesdecreased by 8.5% to €73.9m in line with our strategy to contain costs.

EBITDA

o EBITDAdeveloped to €44.4m in 2Q16, posting a significant increase of 17.1% compared to 2Q15. EBITDA in 1H16 shaped at €88.9m, increased by 10.9% y-o-y.

o Constant currency basis: In 2Q16 EBITDA net of a negative FX impact of €6.2m reached €50.6m (+33.4% y-o-y), while in 1H16 EBITDA net of a negative FX impact of €12.1m shaped at €101.0m (+26% y-o-y).

EBT / NIATMI

o EBT in 2Q16 was shaped at €9.4m compared to €5.4m in 2Q15. In 1H16 EBT was €19.6m from €25.7m in 1H15 (€-6.1m), negatively affected by increased Exchange differences of €8.9m in 1Η16.

o Constant currency basis: In 2Q16 EBΤnet of a negative FX impact reached €14.3m (+70.0% y-o-y), while in 1H16 EBT net of a negative FX impact shaped at €33.6m (+68.6% y-o-y).

o NIATMI from continuing operations in 2Q16 was shaped at €-6.0m compared to €-15.9m in 2Q15, while in 1H16 it was €-15.9m from €-22.7m in 1H15.

o Constant currency basis: NIATMI from continuing operations in 2Q16 net of a negative FX impact reached €-5.2m from €-12.9m in 2Q15, while in 1H16 it was shaped at €-10.2m from €-28.0m in 1H15.

CASH-FLOW

o Operating Cash-flow morethan doubled in 1H16, at €86.2m vs. €41.8m in 1H15. The growth is mainly attributed to the WC improvement (+1.4m in 1H16 from -30.7m in 1H15).

o Net Capexin 1H16 was €26.4m, compared to €34.4m in 1H15. Major Capex items in 1H16 include investments in our US business of €9.7m and R&D of €3.8m.

o Net Debt from continuing operationsin June 2016 developed at €510.8m from €486.8m in March 2016 on a like-for-like basis. Excluding the €13.6m capital contribution to the Italian entity as a result of the M&A transaction Net Debt increased by €10.4m due to dividend outflows to JV partners and FX valuation at the end of June 2016.

o We have in the past engaged in repurchases of our debt and may do so again in the future subject to market conditions. In particular, we are currently reviewing alternatives to refinance a portion of our debt (some or all of our 2018 notes and our syndicated credit facility) as part of our continuous strategy to maintain a strong financial profile and to extend the maturity of our indebtedness. There can be no assurance that any such refinancing may occur in the near future.

o As of 30.06.2016 we held €48,3m of the 2018 bond and €11,3m of the 2021 bond, a total of €59.6m in nominal values.

APPENDIX

o Revenues from Operation contracts (licenses) slightly decreased by 0.5% mainly due to lower revenues in Azerbaijan, Jamaica, Argentina and Brazil partially counterbalanced by the improved performance of Bulgaria, Malta and Cyprus.

o Sales from Management contracts posted an increase of 17.4% mainly driven by the performance of Turkey and Morocco.

o Revenues from HW sales and facilities management increased by 11.4% mainly due to increased revenues in US, partially counterbalanced by the revenues in Argentina, an IT contract in Malaysia and the revenues from the Hellenic Lotteries.

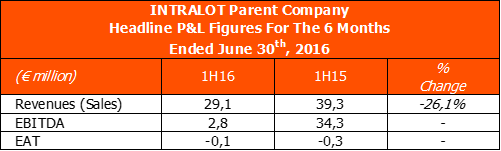

INTRALOT Parent company results

Revenues for the period decreased by 26.1%, to €29.1m.

EBITDA decreased to €2.8m from €34.3m in 1H15.

Earnings After Taxes (EAT) shaped at €-0.1m from €-0.3m in 1H15.

About INTRALOT

INTRALOT, a public listed company established in 1992, is a leading gaming solutions supplier and operator active in 54 regulated jurisdictions around the globe. With €1.91 billion turnover and a global workforce of approximately 5,100 employees in 2015, INTRALOT is an innovation – driven corporation focusing its product development on the customer experience. The company is uniquely positioned to offer to lottery and gaming organizations across geographies market-tested solutions and retail operational expertise. Through the use of a dynamic and omni-channel approach, INTRALOT offers an integrated portfolio of best-in-class gaming systems and product solutions & services addressing all gaming verticals (Lottery, Betting, Interactive, VLT). Players can enjoy a seamless and personalized experience through exciting games and premium content across multiple delivery channels, both retail and interactive.

For more info: Ms. Dimitra Tzimou, Corporate Relations Manager, Phone: +30-210 6156000, Fax: +30-210 6106800, email: tzimou@intralot.com- www.intralot.com